Chinese News Coverage of Latin America

Chinese media coverage of Latin America in February focused primarily on opposition protests in Venezuela.

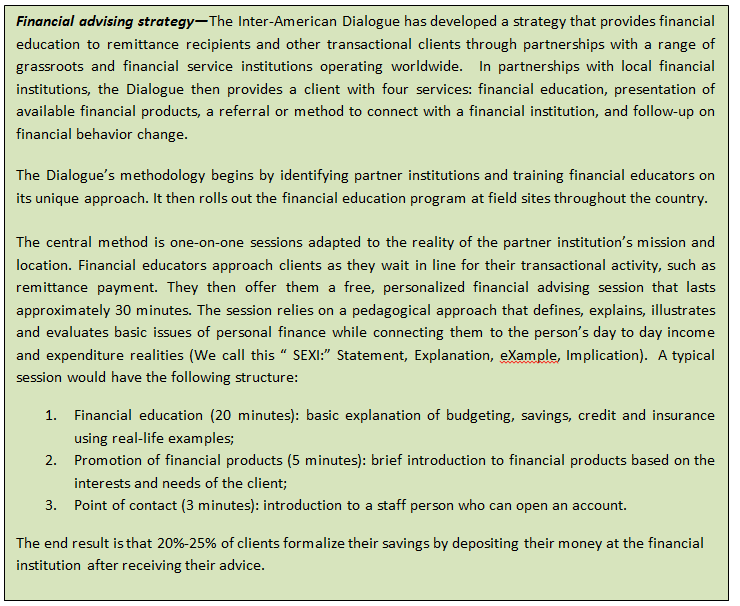

This article analyses financial access in El Salvador, delving into its characteristics and determinants. The article also presents the impact of a financial inclusion strategy to increase savings formalization rates among the population.

The analysis is based on a financial advising project for more than 17,000 Salvadorans at branches of the Salvadoran Credit Union Federation (FEDECACES) located throughout the country. Participants received personalized, 20-minute sessions on personal and household finances, financial products, and options to formalize their savings. During the financial advising session, information is shared and exchanged. On an individual level, this information helps the financial educator orient the information being shared to the needs and interests of the client. On an aggregate level, this presents a fascinating picture of financial access in El Salvador.

The results of the project show that most Salvadorans live on less than US$4,000 a year. Though two thirds of Salvadorans save in some form, they generally lack access to financial institutions, and the result is that the majority of people save informally. Only a very small portion of the population has a savings account or another type of financial product. More importantly, women, homemakers and students, are among those with particularly low financial access.

However, when people receive dedicated, one-on-one financial advising, 15% formalize or increase their savings on the spot. Moreover, when they are prompted to feel a sense of gratitude, the number of people formalizing their savings doubles. Those receiving remittances in particular respond more to the motivation to formalize their savings.

The population served by the project was located in 155 out of a total of 262 municipalities in El Salvador. The credit unions where the project took place are located in places where migration and violence is prevalent, but levels of human development are quite low. The participating towns, those with FEDECACES locations, included 78% of the total population of the country and 79% of all students enrolled in schools. On a darker note, those municipalities also experienced 81% of homicides nationwide. The human development index for participating towns was below average for the country.

Table 1: Population, school enrollment, homicides, development and migration of FEDECACES localities

El Salvador is a low-income economy that has experienced a large outflow of labor migration and a substantial inflow of family remittances from more than one million migrants, mostly living in the United States. The causes of such migration are mixed, and have to do with issues related to economic performance, inequality, insecurity and consolidated migrant transnational networks. The inflow of remittances has contributed to increase their savings. Overall, however, the population continues to experience low earnings.

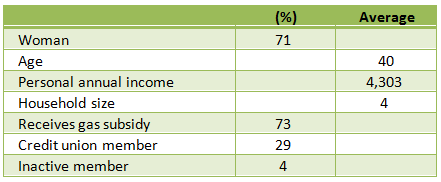

The tables below provide additional detail on the socio-demographic profile of participants, including gender, age, income, and remittance dependence.

The majority of individuals who visit the credit union are what can be called transactional clients, people who go to the credit union to collect a government-issued gas subsidy, to receive a remittance transfer, to pay bills, or to deposit money. In fact, only 29% of people are actual members of the credit union; the rest are visiting the location for transactional activities.

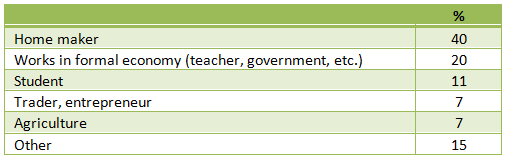

These clients are in their majority women, many of them homemakers, followed by people working in the formal economy, and students. They are in their early forties, with nearly two thirds having a relative living abroad, and half of all clients receiving remittances.

Their income is about US$4300 a year on average, but it is lower among women ($3800) than men ($5222).

Table 2: Socio-demographic characteristics

Table 3: Occupation

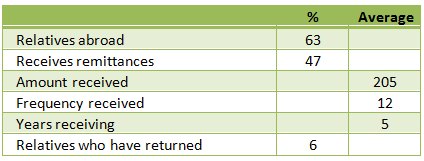

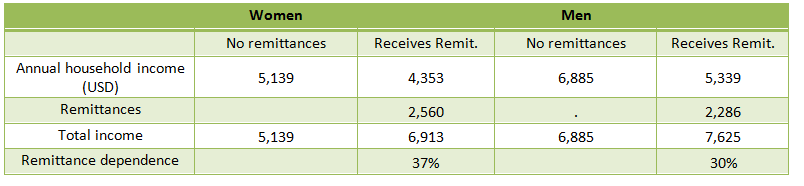

Over sixty percent of participants have relatives abroad, and nearly fifty percent receive remittances. Women tend to be more remittance dependent, first because 49% of them receive remittances compared to 34% of men. And second, their total income includes more remittances than men’s income. On average, participants receive $205 twelve times a year, as the table below shows.

Table 4: Migration and remittances

Table 5: Gender and Remittances

The profile of this population speaks to a low-income society. In El Salvador, income is determined by structural as well as emerging factors such as those associated with migration, like remittances. The fact that 47% of clients that visit Fedecaces branches receive remittances is not accidental given the large migration outflows that have shaped this country’s recent history.

Income among Salvadorans is greatly influenced by age, gender, household size, and financial capability. For example, older people are less likely to have higher earnings. Moreover, gender and financial access are key issues under consideration. Women, and homemakers in particular, are more likely to have lower earnings than men (See Appendix, Table A1).

Those who are able to save, own financial products and receive remittances will have higher incomes than those who don’t share those three features. However, owning financial products is a challenge.

Although income is determined by certain financial endowments, such as savings, financial product ownership or transactions such as family remittances, most Salvadorans have poor financial access.

For example, as mentioned above, only 29% of all people that visit a credit union are actually members. The remaining 70% are what we have called transactional clients.

Second, among transactional clients, the extent of financial access, including ownership of financial products like savings, is very low. They may be able to visit the credit union and enjoy geographic access, but they do not exhibit ownership of financial instruments. For example, only 18% of clients had access to a savings account, the most common type of financial product.

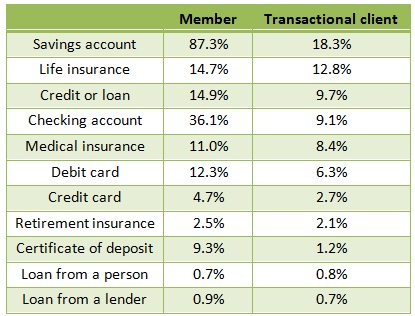

Aside from having a savings account, a much smaller number of people have other financial services, including credit, credit or debit cards or various types of insurance products.

The table below identifies the extent of financial product ownership among credit union members and transactional clients. As the table shows, practically 2 in ten people have savings accounts, and then 1 in ten some kind of credit or insurance.

Table 6: Type of financial products owned

Savings may be related to income and remittances, but are not guarantee of financial access because most money may be informally stored outside the financial system. For example, the percentage of remittance recipients who formally save (47%) is larger than that of non-recipients who formally save (36%). However, the number of people who save in any form is as high among remittance recipients (72%) as non-recipients (75%).

Part of what makes the difference are certain key factors that contribute to greater financial capability or strength. Research has shown that above-average income, having savings in a certain amount, and knowing about personal finances contributes to financial strength. But being a woman and a homemaker makes it harder to have access to financial products.

The data from El Salvador project, in fact, showed that to be the case. Homemakers reported 25% lower rates of financial access than other groups, and even having savings in any form may decrease product ownership, (See Appendix, Table A2). Increases in income and knowing about personal finances (such as knowing to budget), on the other hand, increases the chances of owning a financial product.

These results are important because in El Salvador, as in many other countries, there is a critical mass of people without financial access, particularly without a savings account.

First, only 28% of people who save have a bank account, and 24% of people who have a budget actually have a savings account.

Second, as the table below also shows, there are serious structural problems related to gender: only 17% of women, who represent 70% of all clients visiting the credit union, owned a savings account.

The percentage was even lower among homemakers, which basically was one in 10.

Table 7: People with savings accounts

Given these facts presented above, increasing financial inclusion should be a matter of social and development policy.

To that effect, FEDECACES established a financial inclusion strategy consisting of providing financial advising to all clients visiting the credit unions.

The results of financial education showed that 26% of credit union members increased their deposits. Financial education also helped bring 8% of transactional clients into the credit union as members and open a savings account.

In total, the volume of savings amounted to US$2 million. .

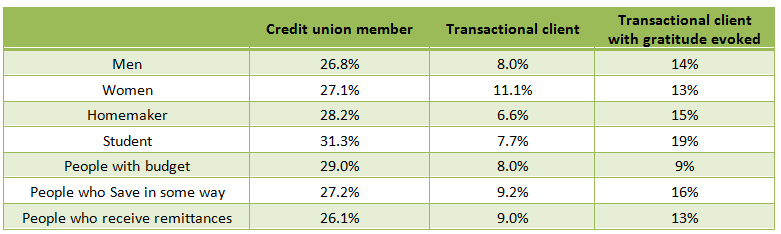

In addition to financial advising, clients were prompted to evoke a sentiment of gratitude at the beginning of the financial advising. In turn, 14% of transactional clients opened a savings account at the credit union. Thus, gratitude increased conversion from 8% to 14% among transactional clients.

About the financial education strategy and its results

The financial education approach consisted of sharing basic knowledge about personal finances with clients. But it also included providing information about financial products offered by the credit union and helping people realize the value-added of formalizing their savings.

The results of this advising approach showed that those who positively demonstrated a commitment to save or use formal financial instruments were more likely to ‘convert’, that is, their commitment increased the chances by 55% to put their money at the credit union at the time of the intervention (Table A3).

In addition, members and clients were asked whether they could evoke a sentiment of gratitude. The results also show that evoking gratitude increased conversion by 58% (Table A3). Those who saved, no matter how much they had, were highly likely to convert. Homemakers showed a positive sign, though not statistically significant, meaning that financial education needs to be differentiated. Students, however, responded to the experiment on gratitude.

Table 8: Percent of people who responded to financial advice

This analysis shows key issues that merit substantive attention. First, Salvadorans exhibit low levels of financial access. In practical terms, although the large majority of Salvadorans save, they do not own a financial product, including a savings account. Second, this situation is more acute among women, and in particular among homemakers. At a large scale, lack of financial access among homemakers is a major policy problem, especially in a country where they amount at least to one quarter of the population and where they already find themselves in financially vulnerable situation.

Third, interventions on financial inclusion are urgently needed, and can positively impact the condition of women and local economies by increasing savings in the financial system. These savings can be then mobilized for credit in key strategic sectors.

Fourth, both the financial advising approach and the gratitude technique are innovative experiences that, now tested, can serve for greater replication and scaling up. To that effect, it is important to set benchmarks and milestones of impact while being mindful of the existing limitations.

Chinese media coverage of Latin America in February focused primarily on opposition protests in Venezuela.

Central America is one of Taiwan’s only remaining diplomatic strongholds.

An op-ed on U.S. support for education in Central America.