How Important is Chinese Lending to Latin America?

Chinese lending to Latin America and the Caribbean hit an all-time high of $37 billion in 2010.

Guatemala’s economic growth and development has historically been affected by high rates of inequality, as well as by a poorly performing economic model that is based on agricultural exports. Due to their fluctuating and low yield, agricultural exports do not lay the foundations for wealth in an economy or a society. Moreover, and largely as a result of this agricultural orientation, the country’s labor force is uneducated (28%), unskilled (33%), underpaid and informal (at least 50%).[1] As a result, many Guatemalans have sought alternative forms of employment, including international labor migration as an employment strategy.

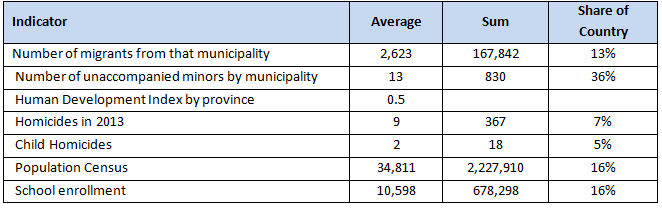

Table 1: Indicators of Migration and Development

Source: Orozco and Yansura, “Understanding Central American Migration: The Crisis of Central American Child Migrants in Context,” Inter-American Dialogue, August 2014.

The links between migration and development

Given the existing circumstances and the presence of a sizable migrant population remitting to nearly 200,000 households, with resources that generate important stocks of savings, it is important to integrate migration into development strategies.

The point of departure in remittances and development is their effect on income. Remittances are typically pooled with other sources of income (salaries, rents, social support). Out of all income earned, remittances included, savings are set aside and built. Because remittances have the effect of increasing disposable income, they also increase the household’s capacity to save. Thus, at the level of the household, remittances contribute to building liquid and fixed assets.[1]

However, it is important to differentiate between formal and informal savings. Remittance recipient households can and do save, but without access to financial institutions and services, much of their savings are kept informally.[2] Moreover, given such informality, their resources are not well managed nor taken advantage of, even in the context of important financial demands, such as investments in education and healthcare.

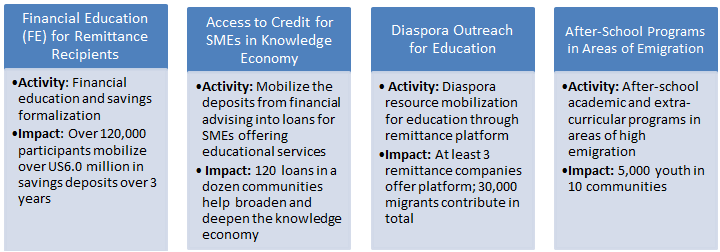

In this context, Opportunities for My Community introduces an innovative, three-year strategy to promote development in Guatemala integrating migration, remittances, savings and education into programs that will enhance wealth and knowledge. The project links migration and development through four components:

This approach is fundamentally important because it addresses various strategic needs. First, it integrates migrant capital investment and savings from remittances into the financial sector, further mobilizing these resources for local development in education and skill formation. Second, this strategy expands and complements—that is, does not replace— existing approaches to economic growth, and creates a new model for much-needed investments in services for the global economy.

Making investments in savings and education as a business strategy will lead to an expansion of opportunities to work and compete in the knowledge economy. This strategy does not compromise existing investments in agriculture but it expands credit to sectors—such as education and skill formation—for which no substantive financing has existed before.[1]

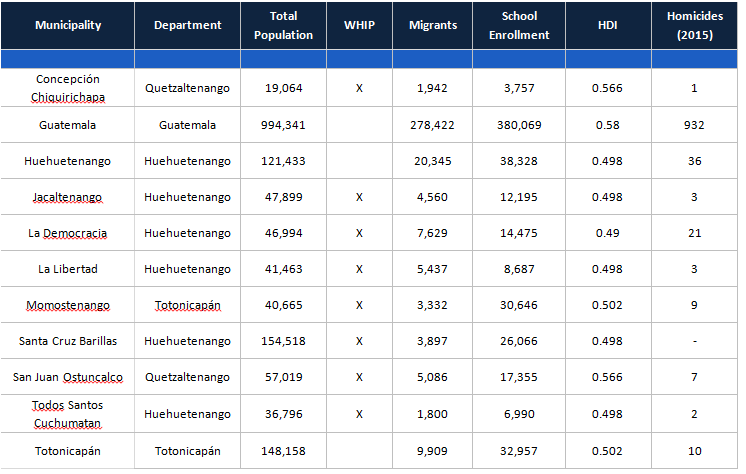

The project focuses on municipalities of the Western Highlands and Guatemala City, locations selected following two criteria: the priority level assigned by USAID’s Western Highlands Integrated Program (WHIP), and emigration levels. In each of these municipalities, work will be conducted in partnership with local financial institutions, schools and NGOs.

Table 2: Selected Municipalities

Source: Orozco and Yansura, “Understanding Central American Migration: The Crisis of Central American Child Migrants in Context,” Inter-American Dialogue, August 2014.

Financial education has proven to be an efficient tool for systematically and effectively building assets in a society.[1] Our financial education project consists of a successful and innovative strategy that promotes financial inclusion, education, and savings mobilization. It forms, informs and converts transactional clients into account holders, bringing their informal savings into the formal financial system.

The project utilizes a strategy with six main components: 1) developing financial sector partnerships; 2) selecting and training of a team of financial educators; 3) providing one-on-one financial advising for remittance recipients and other transactional clients; 4) conducting workshops and trainings for financial institution staff; 5) tracking data and outcomes; and 6) sharing outcomes and lessons-learned with stakeholders.

Our goal is to reach over 120,000 people and bring at least 20,000 (or over 15%) into the formal financial system, formalizing an estimated $6 million in savings. The expected results are to establish and modify behavior and knowledge on basic financial management. Establishing new behavior and knowledge motivates thinking about saving and budgeting, and modifying behavior and knowledge mobilizes personal resources into the formal financial system. Thus, we achieve financial access and education simultaneously.

This second and parallel initiative will engage our partner financial institutions in reinvesting into the local community in the form of credit. This will entail mobilizing deposits from the financial education portion of the project, as well as deposits from the bank’s larger portfolio, into loans for entrepreneurs, particularly [though not exclusively] those in the knowledge economy.

The goal is to reach entrepreneurs in need of financing, as well as those in the knowledge economy, in order to promote their growth and widen their impact. These enterprises might include data management services, internet cafes, education and tutoring services, and foreign language classes. This sector is extremely important for expanding from the agroexport-driven economy to the knowledge-driven economy, providing much needed resources for human capital development.

Our aim is to finance about 120 entrepreneurs, at least half of whom are working in the educational/knowledge services sector, with loans averaging $6,000/enterprise.

This third initiative consists of diaspora outreach for education in Guatemala. This investment will complement the activities described in previous components. The purpose of this component consists of promoting diaspora and private sector partnerships in education; in other words, it aims to motivate and mobilize diaspora resources using existing money transfer interfaces.

Our research has shown that there is a critical demand among migrant remittance senders to invest in education and workforce development (the typical recipient household has at least one child enrolled in K-12 education, and one adult in the workforce), and that they are prepared to mobilize their savings toward that end.

In order to satisfy this demand, we will develop a partner initiative that creates incentives for migrants to invest in education using the already-existing remittance service platform of MTOs that belong to the Remittance Industry Observatory (RIO).[2]

The investment in education strategy consists of crafting a relatively low-cost outreach campaign that attracts migrant donations for educational services (such as existing educational programs for high school youth) and transfers the donations through MTO sending channels. The campaign and donations will use MTO networks to support projects in ten communities in Guatemala.[3]

The investment initiative will seek to reach out to 10% of Guatemalan remitters, including the highland area. This strategy is achievable because RIO members perform more than 50% of the total market of remittances to the country—that is, more than 400,000 transactions a month. The goal is to promote donations from approximately 10,000 migrants, representing a critical mass needed for a successful initiative. We expect the amount of donations to vary from person to person and to promote the mobilization of US$150,000 to be invested in education projects in Guatemala during its first year of operation.

This fourth component provides a strategy for strengthening human capital among youth in high-emigration areas, specifically by expanding access to high-quality after-school programs. This component, which is closely linked to Diaspora Investment in Education, will offer after-school programs during the second and third years of the overall initiative.

Working in the same communities where migration has occurred, and where the other initiatives are taking place, we will expand access to after-school programs while also strengthening curricular content and learning outcomes for these programs. Specifically, working in partnership with local schools, NGOs, and parent groups, we will provide after-school education to at least 5,000 students in at least ten communities during the three-year period. The objectives of this project are to keep kids off the streets, to retain them in the educational system, and to improve their learning outcomes.

[1] OECD (2005), Improving Financial Literacy: Analysis of Issues and Policies; OECD (2008), Financial Education and Awareness on Insurance and Private Pensions. OECD (2011); Orozco, Manuel. (2010).

[2] RIO is an Inter-American Dialogue initiative involving more than a dozen remittance service providers, including banks and MTOs, that promotes dialogue among remittance industry leaders and development practitioners. It also shares information on key trends and engagement on development issues. For more information, see https://www.thedialogue.org/page.cfm?pageVersion=working&pageID=767

[3] A money transfer company can offer customers the opportunity to donate a dollar to their city’s education program when they make their remittance transfer. There would be no additional cost for the added donation. The company can promote the donation in the same way that they advertise free money transfers for humanitarian reasons.

[1] Financing for education is typically only available for college education in private universities. However, financing education is key to economic growth and development.

[1] For a more detailed discussion, see Orozco, Manuel. “Remittances and Assets: conceptual, empirical and policy

considerations and tools.” UNCTAD, 2012. Available at https://www.thedialogue.org/PublicationFiles/UNCTAD-Maximizingdevelopmentimpact.pdf

[2] In some cases, remittance recipients face geographical, social, or legal barriers that make it very difficult for them TO? access a financial institution. Even those who have access may not use financial institutions and services because they do not realize that they have access, or because they do not understand the benefits of using them. For example, many remittance recipients enter financial institutions on a monthly basis to receive their remittance, but do not hold a savings or checking account with that institution. In light of this, financial access and financial education can help to mobilize remittance recipients’ informal savings into the formal financial sector.

[1] OIT. Evolución de los principales indicadores del Mercado de trabajo en Centroamérica y Republica Dominicana, 2006-2010. 2011.

Chinese lending to Latin America and the Caribbean hit an all-time high of $37 billion in 2010.

Venezuelan president Nicolas Maduro left China last month with a supposed show of support from the Chinese government.

Summary of PREAL’s recent international conference on teacher effectiveness, held in Guatemala City.