PREAL International Conference 2010: Teacher Effectiveness

Summary of PREAL’s recent international conference on teacher effectiveness, held in Guatemala City.

For the many Guatemalan families that receive remittances, the extra money coming in helps increase disposable income and makes it easier to save money. Unfortunately, without access to financial institutions or information on personal finance, much of these savings are kept “under the mattress,” or informally. Bringing these resources to the financial system in savings is vital. Not only does it help households build wealth, it can also be leveraged for economic growth at the community level, boosting the local economy through increased resources available for investment.

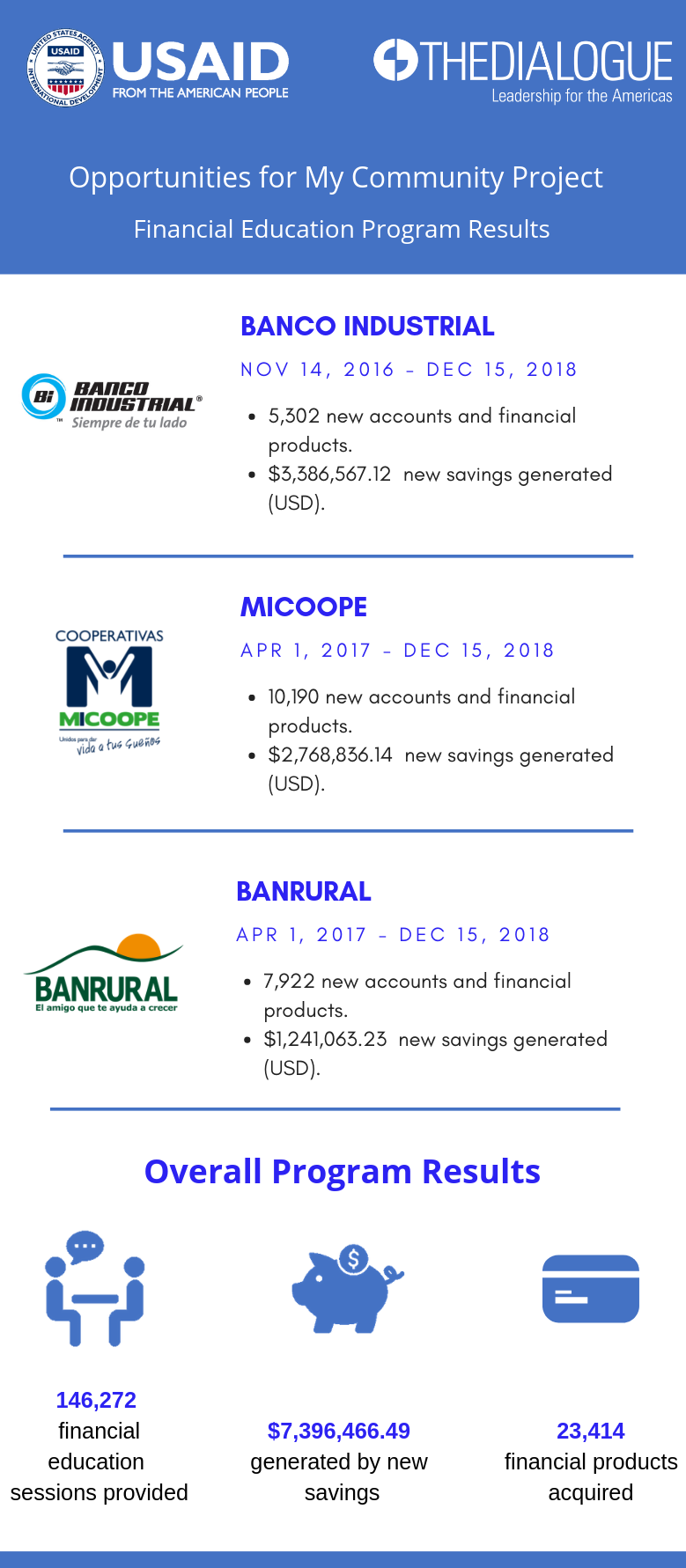

Responding to this need, the Opportunities for My Community Project implemented a successful two-year financial education program in partnership with MICOOPE, Banco Industrial and Banrural, three major financial institutions in Guatemala. The program was open to everyone; however, it had a special focus on remittance recipients, who have a strong potential to save money due to their increased levels of disposable income.

Financial education is a useful tool for promoting economic development. Unfortunately, many people in Guatemala do not have basic knowledge of personal finance, which creates barriers that limit their access to financial institutions and products, and over the long term reduces their ability to save and invest.[1] Through financial education, people can achieve greater financial independence[2] and improve their quality of life.

The program consisted of an innovative strategy to promote financial inclusion and savings mobilization. Working with a team of 30 financial educators, the project provided personalized financial advising sessions in selected bank and credit union branches located in the Guatemalan Western Highlands and Guatemala City.

Through these sessions, participants learned the basics of personal finance, including saving and budgeting. They also learned practical things such as how to open an account and the factors to consider before doing so. Armed with new information and skills, participants have been empowered to improve their personal financial habits.

From November 14, 2016 to December 15, 2018, the project held 146,272 individualized financial education sessions. Among participants, more than half were from Mayan ethnic groups and 63 percent were women, two population groups that have been historically marginalized in Guatemala.

Furthermore, the project data shows that 41.6 per cent of people advised were remittance recipients, of which 8 out of 10 reported that they were actively saving money. Among remittance recipients who report saving money in some way, the average stock of savings is Q18,186 ($2,424.8), almost twice as much money as those who do not receive remittances (Q9,320 or $ 1,242.7). These figures demonstrate remittance recipients’ high potential to save money, build financial assets, and contribute to economic development in their community.

The overall program results have been remarkable, with 27.47 per cent of participants formalizing their savings, either by making a deposit, opening an account, reactivating an account, or acquiring another product such a credit or an insurance policy.

Moreover, as a result of the financial advising, over 23,400 new financial products were acquired by the participants, mobilizing more than USD $7,350,000 in informal savings into the formal financial sector. Formal savings have several important benefits: participants can earn interest, better manage their money, and have access to a wide variety of financial products.

The benefits of these resources can be seen at both the community and the individual level. With regards to the former, thanks to the financial education sessions provided by the project, these resources can be better invested through the formal financial system, creating more economic opportunities in Guatemala by integrating and mobilizing them to promote local development. To put it more simply: when savings are kept at banks or credit unions, they open up more opportunities for loans and investments, which is important for economic development.

Financial education sessions have also helped participants build good financial behaviors, including seeing the value of budgeting, saving, and planning for the future. They have also opened their own savings account and acquired, according their needs and situation, other financial products such credit or insurance. All of this contributes to their financial inclusion, empowering them to have greater agency over their personal finances to ultimately improve their financial situation.

Summary of PREAL’s recent international conference on teacher effectiveness, held in Guatemala City.

Links to agenda and media coverage of a conference on the state of the teaching profession in Guatemala.

Business and education leaders discuss business sector engagement in education reform in Latin America.